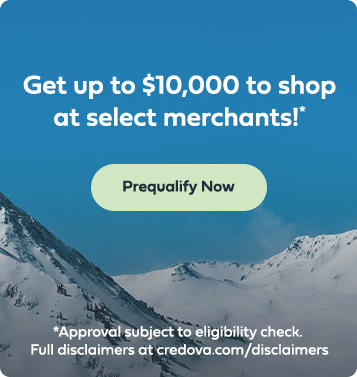

Adventure now, Pay later

Buy now, pay later for the outdoor lifestyle

Get approved for up to $10,000 without affecting your credit.

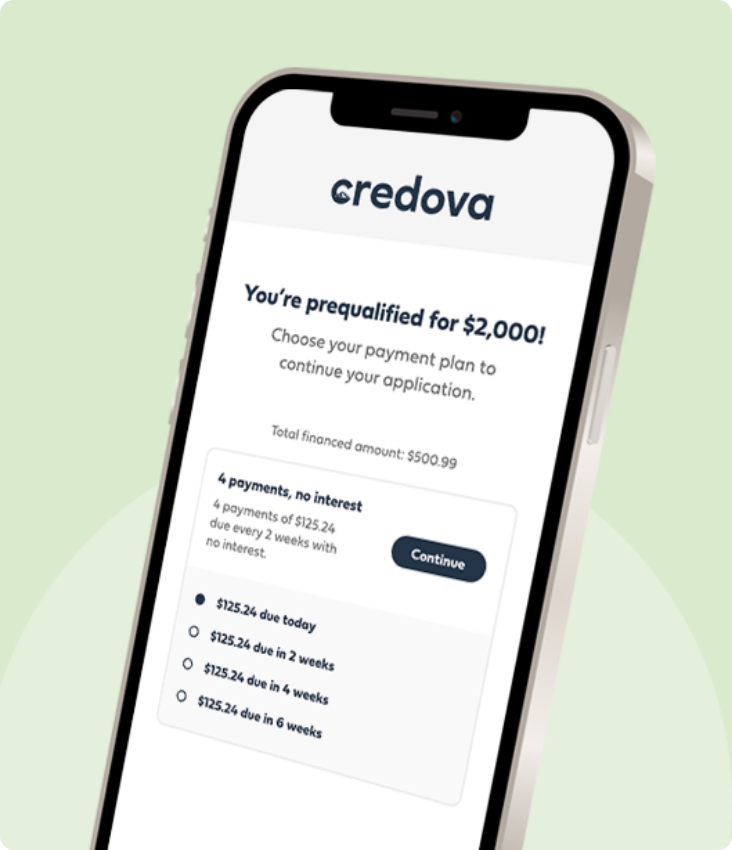

No hard credit inquiries

Get approved without any

impact to your credit.

4 interest-free payments

Just 4 payments and no interest.

Shop today

Get approved and use your approval in-store and online.

No hard credit inquiries

Get approved without any

impact to your credit.

4 interest-free payments

Just 4 payments and no interest.

Shop today

Get approved and use your approval in-store and online.

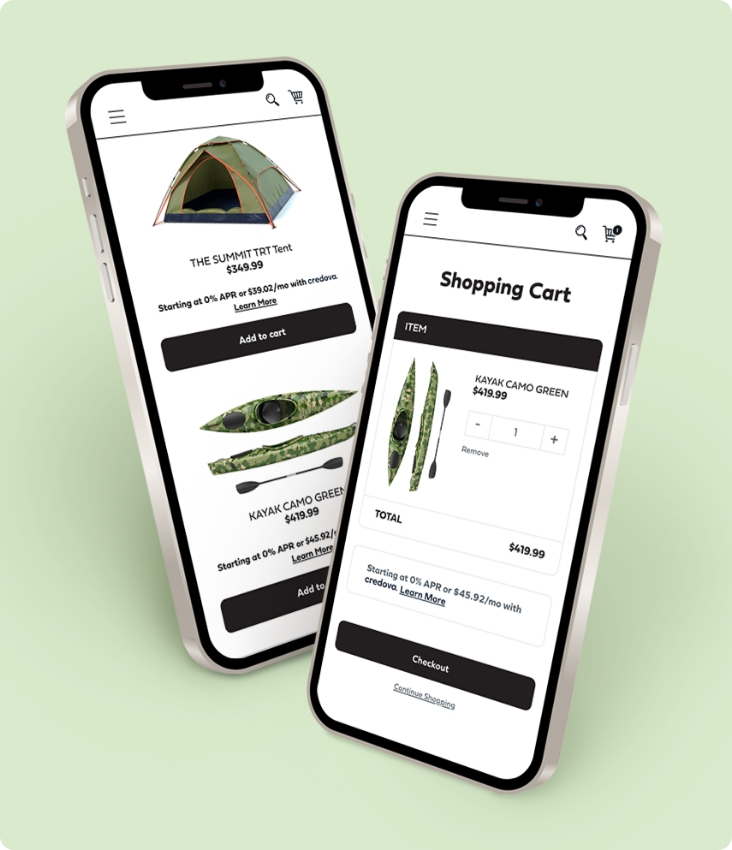

How it works

Start your adventure with Credova

STEP 1

Fill your cart

Shop your favorite stores and

then select Credova at checkout.

STEP 2

See how much you can spend

Get approved without affecting

your credit score.

STEP 3

Pay over time

Select Credova at checkout to

pay for your purchase over time.

For Shoppers

Ready, set, go! Get outside and get exploring today with Credova.

For Business

Give your customers the buy now, pay later options they want. Start here.

Credova reviews

Cody I

“One of the easiest financing programs I've ever used. I would highly recommend Credova.”

Thomas M

“Easy approval with financing or lease options. I've used them at least 3 times. I always pay off during the no interest period. I really like that option.”

Melinda K

“Really want a product Bud's carried but didn't have all the money at once so I used this service and they have been fantastic. I would recommend them to everyone. Thanks again”

Enrique O

“Credova gave me an opportunity to own products that I would not have been able to afford if I had to pay for them outright in full. With the option to pay in 90 days same as cash, I saw it as a no brainer. I'll continue doing business with Credova as long as they're willing to keep providing these unique opportunities.”

GJ H

“Great customer service. I had to change the seller several times because the item I wanted would sell out so fast. Each time I called Credova, the agent was friendly, knowledgeable, and helpful. Great customer service. Fast approval. Highly recommended!”

EW II

“Good so far had some hang ups with the software from my and called they walked me through the whole process and it lets me keep a lot of money in my pockets while I have the gun...AWSOME SAUCE!!! THANKS CREDOVA!!!”

Courtney B

“I have no complaints. Great company and the bank they associate with Monterey financial I believe it is. Paid my loan back early and they gave me a pre-approval 3 days after I paid it off. And I just opened another line of credit a couple days ago. No complaints at all.”

Lawrence H

“This is the fourth time I have used Credova and I will continue too!! Easy and hassle free!”

EB

“Was able to make a purchase using their services. Without them I may not have been able to get the item I wanted. Customer service was great as well. Needed assistance switching merchants upon completion of first purchase attempt; item was not exactly what I needed from first merchant. Once purchase is made a Credova associate must release funds/ contract for use at another merchant. This process worked seamlessly for me. Thank you, Credova.”

David P

“Fast approval, easy to understand terms and conditions, and easily accessed on the retailer's site when checking out! Thumbs up from me.”

Luis R

“Approved right then and there, but what I liked was the questions they asked just to make sure I was who I said I was. Felt secured and I would definitely use again.”